The ability to understand the financial statements of a company is one of the most vital skills for investors, entrepreneurs, or even managers. With the information they can read and understand, investors can better identify promising opportunities while avoiding unwanted risk. Entrepreneurs and professionals can also make more strategic business decisions. Financial statements offer a view into the financial health of a company.

To understand a company’s financial status, you will need to look at several financial statements: balance sheets, income statements, cash flow statements. They are usually made available by the company itself and are part of the different reports a company will publish for a specific time frame (annually, quarterly...). The value of these documents lies in the story they tell when reviewed together.

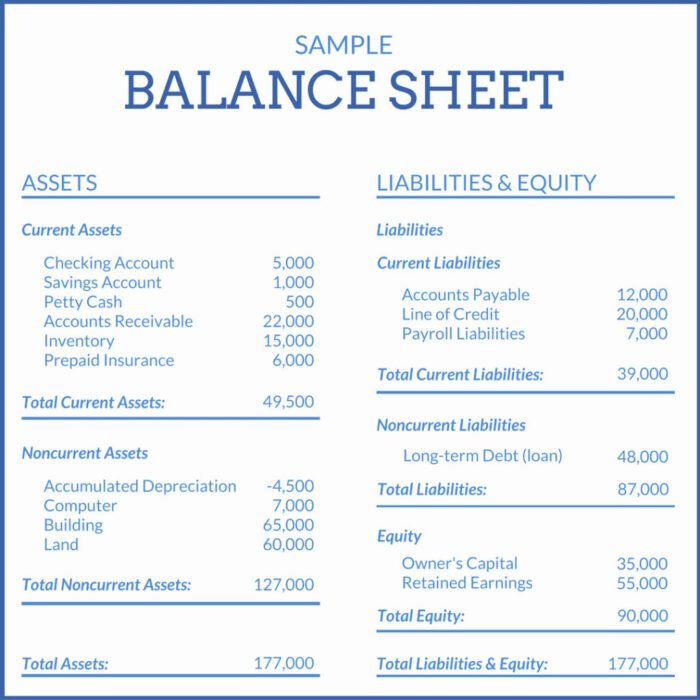

1. How to Read a Balance Sheet

A balance sheet conveys the “book value” of a company. It allows you to see what resources it has available and how they were financed as of a specific date. It shows its assets, liabilities, and owners’ equity (essentially, what it owes, owns, and the amount invested by shareholders).

The balance sheet also provides information that can be leveraged to compute rates of return and evaluate capital structure, using the accounting equation:

Assets = Liabilities + Shareholders’ Equity

Liabilities = Assets -Shareholders’ Equity

Assets are anything a company owns with quantifiable value.

- Current assets are also referred to as short-term assets. These are typically liquid, or likely to be realized within 12 months. Here are some examples.

- Cash and equivalents, including your business checking account balance

- Accounts receivable and any short-term invoices you’re owed

- Inventory including goods for sale, raw materials and items being made

- Expenses you have paid in advance, such as rent or business insurance

- Non-current assets or long-term assets, include investments and other less tangible assets which nonetheless can bring value to your business. Take a look at these examples to give you an idea of what to include.

- PP&E — this stands for property, plant and equipment, and is usually shown net of depreciation

- Intangible assets such as trademarks, patents, copyright and goodwill

Liabilities refer to money a company owes to a debtor, such as outstanding payroll expenses, debt payments, rent and utility, bonds payable, and taxes.

- Current liabilities are the items a company owes in the next year, and can include things like unpaid supplier invoices, or upcoming repayments for debts you’ve committed to like business loans. You can expect to include items like these:

- Accounts payable — also known as AP, the debts you owe to suppliers or to cover anything else bought on credit

- Current debt/notes payable, which covers all non-AP bills you’ll need to pay in the coming 12 months, like payroll expenses, rent ...

- Current portion of long-term debt, so the amount you need to pay back in the next year, from any long term liabilities like a mortgage or business loan

- Non-current liabilities means any long term liabilities. Here are a couple of examples.

- Company-issued bonds

- Long-term debt such as a mortgage, including the principal amount left to repay and any interest which will be added

Shareholders’ equity refers to the net worth of a company. It’s the amount of money that would be left if all assets were sold and all liabilities paid. This money belongs to the shareholders, who may be private owners or public investors.

- Owner’s investments in a business

- Share capital if the company has been investor funded

- Retained earnings, where the business has decided not to issue all profits as dividends, but has held some itself to reinvest

Alone, the balance sheet doesn’t provide information on trends, which is why you need to examine other financial statements, including income and cash flow statements, to fully comprehend a company’s financial situation.

2. How to Read an Income Statement

An income statement, also known as a profit and loss (P&L) statement, summarizes the cumulative impact of revenue, gain, expense, and loss transactions for a given period. The document is often shared as part of quarterly and annual reports, and shows financial trends, business activities (revenue and expenses), and comparisons over set periods.

Total Revenues - Total Expenses = Net Income

Income statements typically include the following information:

- Revenue: The amount of money a business takes in

- Expenses: The amount of money a business spends

- Costs of goods sold (COGS): The cost of component parts of what it takes to make whatever a business sells

- Gross profit: Total revenue less COGS

- Operating income: Gross profit less operating expenses

- Income before taxes: Operating income less non-operating expenses

- Net income: Income before taxes less taxes

- Earnings per share (EPS): Division of net income by the total number of outstanding shares

- Depreciation: The extent to which assets (for example, aging equipment) have lost value over time

- EBITDA: Earnings before interest, taxes, depreciation, and amortization

Accountants, investors, and other business professionals regularly review income statements:

- To understand how well their company is doing: Is it profitable? How much money is spent to produce a product? Is there cash to invest back into the business?

- To determine financial trends: When are costs highest? When are they lowest?

3. How to Read a Cash Flow Statement

The purpose of a cash flow statement is to provide a detailed picture of what happened to a business’s cash during a specified duration of time, known as the accounting period. It demonstrates an organization’s ability to operate in the short and long term, based on how much cash is flowing into and out of it.

Cash flow statements are divided into three sections:

- cash flow from operating activities: details cash flow that’s generated once the company delivers its regular goods or services, and includes both revenue and expenses.

- cash flow from investing activities is cash flow from purchasing or selling assets—usually in the form of physical property, such as real estate or vehicles, and non-physical property, like patents—using free cash, not debt.

- cash flow from financing activities: details cash flow from both debt and equity financing.

It’s important to note there’s a difference between cash flow and profit. While cash flow refers to the cash that's flowing into and out of a company, profit refers to what remains after all of a company’s expenses have been deducted from its revenues. Both are important numbers to know.

With a cash flow statement, you can see the types of activities that generate cash and use that information to make financial decisions.

Ideally, cash from operating income should routinely exceed net income, because a positive cash flow speaks to a company’s financial stability and ability to grow its operations. However, having positive cash flow doesn’t necessarily mean a company is profitable, which is why you also need to analyze balance sheets and income statements.

A positive cash flow indicates that a company has more money flowing into the business than out of it over a specified period. This is an ideal situation to be in because having an excess of cash allows the company to reinvest in itself and its shareholders, settle debt payments, and find new ways to grow the business. Positive cash flow does not necessarily translate to profit, however. Your business can be profitable without being cash flow-positive, and you can have positive cash flow without actually making a profit.

Having negative cash flow means your cash outflow is higher than your cash inflow during a period, but it doesn’t necessarily mean profit is lost. Instead, negative cash flow may be caused by expenditure and income mismatch, which should be addressed as soon as possible. Negative cash flow may also be caused by a company’s decision to expand the business and invest in future growth, so it’s important to analyze changes in cash flow from one period to another, which can indicate how a company is performing overall.

Don't forget to follow JumpFinance on:

- Youtube

Comments

Post a Comment